The Plasma Value Chain is Complex

Plasma derivatives are a specialized category of biopharmaceutical products extracted from human blood plasma through sophisticated fractionation processes. These life-saving therapeutics serve as critical interventions for patients with rare, chronic, and often life-threatening conditions where conventional pharmaceutical approaches fall short.

Examples of Products include — Albumin, Immunoglobulins, Clotting Factors, etc.

The Value chain is long and involves highly specialized collection and complex manufacturing processes which require a high degree of Quality control and consequently the derived product have a high regulatory barrier to market entry.

Below table captures the key product categories :

The specialized manufacturing processes and strict regulatory requirements for plasma derivatives create substantial barriers to entry in this sector. Each step of the value chain — from plasma collection through testing, fractionation, formulation, and distribution — demands specific expertise and infrastructure investment. The biological nature of the source material necessitates rigorous quality management systems to ensure product quality and patient safety. These fundamental characteristics of plasma production have shaped a global market with distinct dynamics, competitive structures, and growth patterns that differentiate it from conventional pharmaceutical segments.

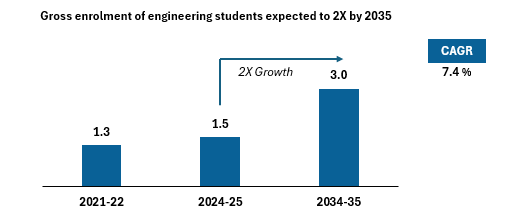

Plasma Derivatives is a Large, Growing Market

Unlike synthetic drugs, plasma-derived products face inherent supply constraints due to their dependence on human donors, resulting in an industry where supply elasticity fundamentally lags demand growth. This structural characteristic has maintained pricing power even during broader healthcare cost pressures.

Market stratification is evident as technological differentiation in manufacturing processes creates demonstrable quality variations. The emergence of chromatography-based purification versus traditional Cohn fractionation has established a two-tier market where premium products command sustainable price advantages of (15–25%) based on superior purity profiles and reduced immunogenicity. This quality-based bifurcation has restructured competitive positioning, rewarding tech leadership rather than merely scale advantages.

Post-pandemic supply chain disruptions have permanently altered the market landscape, with collection volumes recovering more slowly than underlying demand. This widening gap between supply capabilities and clinical requirements has transformed inventory management into a priority for and manufacturers with secured plasma supplies have a great foothold in the market.

The Indian Market is an Outlier

A few key factors make India a unique market in the context of plasma derivatives:

1. For a few product categories like IVIG, Albumin, the market is majorly catered to by domestic players — with nearly ~100% of IVIG and ~80–90% of the Albumin market being serviced by domestic players

2. Clinical adoption: The awareness, and consequently usage of many plasma derived products is still very low in India. For instance, in clinical situations where the use of anti-coagulants is warranted, most clinicians do not test for an anti-thrombin 3 deficiency. The presence of this deficiency in the patient means that the widely accepted standard of care in anti-coagulants — Enoxaparin, Heparin, etc. will simply not work! The fact that most doctors are unaware of the need to test for such a critical deficiency, and that there are much better product alternatives (plasma derived anti-thrombin 3) is one instance among others that shows that India still has a lot of ground to cover in this regard

3. Senior executives point out that the fragmented collection ecosystem and absence of clear incentives for voluntary donations constrain domestic production economics. Coupled with high compliance costs for GMP-certified facilities, this limits the entry of new fractionators.

Key Factors Driving Growth of the Market

The market continues to grow on the back of a few key drivers –

1. Aging Global Population directly impacts plasma derivative demand through increased prevalence of immunodeficiency conditions and higher surgical intervention rates. With the global population over 65 projected to increase from 9.3% to 16.0% by 2050, utilization of immunoglobulins and albumin is expected to rise proportionally. Clinical data demonstrates that patients over 65 require immunoglobulin therapy for primary immunodeficiency at ~ 2.3x the rate of younger populations

2. Expanded Treatment Protocols across medical specialties have broadened the application of plasma derivatives beyond traditional indications. There has also been more widespread use of Off-Label Use. These established but relatively recent applications have increased immunoglobulin utilization globally

3. Technological Improvements in Manufacturing have substantially increased protein recovery rates from collected plasma. Modern chromatography-based fractionation methods achieve 25–30% higher yields for key proteins compared to traditional Cohn precipitation techniques. This enhanced efficiency effectively expands available supply from existing plasma collection volumes while reducing production costs per gram of protein recovered

4. Limited Substitution Potential from biosimilars or alternative therapeutics has largely preserved the market position of plasma derivatives. Despite decades of research, recombinant alternatives have achieved meaningful market share only in specific coagulation factors, with other plasma proteins proving exceptionally difficult to replicate through non-plasma-derived methods

India’s plasma derivatives market is positioned for gradual but meaningful progress. Demand continues to grow across key therapeutic areas, while clinical adoption patterns are becoming more standardized. The immediate priorities are operational: improving donor recruitment and retention, strengthening cold chain infrastructure, and streamlining regulatory processes. Over the medium term, establishing reliable domestic fractionation capacity will reduce import dependence and price volatility. Success will require coordinated efforts between government policy, healthcare institutions, and industry players.

LoEstro Advisors is an investment banking firm specializing in sell-side fundraise and M&A advisory, along with a strong consulting arm.

Over the last four years, we have grown to be one of India’s largest (in terms of M&A transactions) homegrown boutique investment banks, with $1billion + worth of combined deals closed across education, healthcare, consumer, and technology sectors.