Healthtech is a broad term that encompasses all of the technologies that are used to improve healthcare delivery. This includes everything from Electronic Health Records (EHRs) to wearable devices to telemedicine. Healthtech is rapidly evolving, and it has the potential to revolutionise the way we deliver health care.

Technological innovation in healthcare has revolutionized the industry, improving patient outcomes and boosting healthcare system efficiency. Owing to it, providers and businesses now offer diverse services alongside traditional medical products.

The advent of technological innovation in healthcare has had a profound impact on the industry, transforming the way healthcare is delivered, improving patient outcomes, and enhancing the overall efficiency of healthcare systems. With the advancement of technology, healthcare providers and businesses have expanded their offerings to include a variety of services that complement traditional medical products.

For example, the “United Health Interface” initiative in India seeks to create a centralized platform that connects various stakeholders in the healthcare ecosystem. This platform would allow individuals to access their comprehensive medical history, diagnostic reports, and treatment plans securely stored in digital health records. By facilitating information exchange between hospitals, clinics, and diagnostic centers, this initiative aims to streamline healthcare offerings and make them more patient-centric.

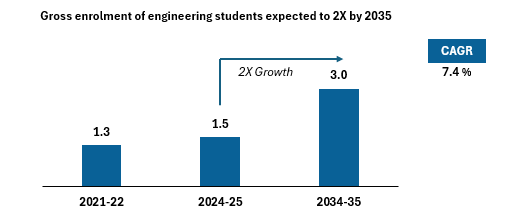

The government of India is trying to develop India as a global hub for healthcare services. The key growth drivers are:

Need for improving accessibility

2. Increasing internet penetration

3. Increase in chronic diseases

4. New innovations and improving affordability

The Indian e-pharmacy market is expected to rise at a 22 per cent CAGR and reach US$1.1bn in market value

Healthtech in India can be segmented into two broad sectors — Curative care and Preventive care. ePharmacies and eDiagnostics account for the biggest market size of US$7,500m in the curative care sector. Online pharmacies include independent internet-only outlets, electronic subsidiaries of “brick-and-mortar” hospitals, and platforms serving pharmacy companies. E-pharmacies are acquiring a major stake in the pharma retail value chain with the major growth drivers being: unorganised nature of traditional pharma retail, governmental support, value and convenience offered and tremendous potential untapped in tier II and tier III cities.

Teleconsultations are revolutionising healthcare access

Telemedicine in India is at a nascent stage compared to developed countries like the USA but that is all set to change. The Indian telemedicine market is expected to rise at a 21 per cent CAGR and reach US$5bn in market value.

India’s rehab-tech market: US$17bn opportunity, set to double in 5 years

Rehab tech comprises interventions that enhance functionality and minimise disability. The services include nursing, caregiving, physiotherapy, occupational therapy, and medical aid equipment. Hospital and local unorganised players are currently the major providers of rehab, however, this is bound to change as rehab-tech players offer a better service.

Despite allocating 91 per cent of funds to curative healthcare, it still faces significant drawbacks and limitations

Lack of healthcare infrastructure such as the shortage of physical infrastructure, including hospitals and beds, remains a challenge in the healthcare system. Both primary and tertiary healthcare centers are limited in number, exacerbating the issue. Furthermore, there is a scarcity of healthcare professionals, including doctors, nurses, and ICU staff. Health literacy is alarmingly inadequate in rural areas. When compared to developed countries, the healthcare system in this context encounters obstacles related to high out-of-pocket expenses, low per capita income, and relatively low government spending on healthcare as a percentage of GDP. These factors impede financial protection, access to high-quality care, and healthcare affordability. By shifting the focus to prevention, there is a greater potential to improve patient outcomes in healthcare.

Market size for preventive health is expected to reach US$197bn at 21 per cent CAGR from 2021–25

Preventive healthcare is taking a front seat in India and rightly so. India’s booming healthtech market is offering diverse services, including corporate partnerships and convenient health insurance options. It also includes lifestyle monitoring features like step count and heart rate tracking, granting access to valuable health data. Additionally, the market covers supplements, nutrition management, and a variety of physical wellness options. Mental and social well-being are addressed through emotional and psychological wellness services, while condition management focuses on structured treatment for chronic diseases, aiming to improve patients’ overall quality of life. Compared to their counterparts in the United States, Indian startups currently face limited funding. However, if India were to take the path of preventive health, there needs to be promising investment opportunities in lucrative markets such as condition management, social and mental wellness, fitness and wellness, as well as supplements and nutrition.

Government fuelling the tech progress

National Health Stack, launched by the National Health Authority of India, is a newly introduced digital health infrastructure aimed at serving as a foundational component for digitising the healthcare sector in the country. The 4 layers that form the National Health Stack are — user applications, unified health interface, health data exchange and other digital public goods.

The user applications, as the final level of the ecosystem, consist of applications and platforms developed by the government or private sector. The unified health interface, similar to NPCI and UPI in India’s payment layer, facilitates seamless interactions between patients and digital health service providers through open protocols and the introduction of the Universal Health ID (UHI). In addition, the health data exchange forms the necessary digital infrastructure modules for ensuring interoperability of different health data types. The foundational base layer leverages existing digital public goods to establish the groundwork for achieving interoperability in digital health services.

According to NITI Aayog the National Digital Health Mission (NDHM) will spur a fundamental transformation in India’s healthcare system and unlock economic value worth over $200 billion by 2030.

Recent trends in the market

Tech is blurring the distinction between D2C and B2B leading to a highly interconnected and patient-centric healthcare ecosystem. Technology has enabled consumers to have direct access to care services while also allowing stakeholders to collaborate. The current and future trends in the healthtech ecosystem are:

Holistic one-stop healthcare: M&As are expected to persist due to increasing consumer demand for integrated healthcare solutions as well as emergence of ‘one-stop-shop’ healthcare models.

Hospital driven integration: With around 65 per cent of medical-clinician talent engaged in public and private hospitals in India, hospitals have an advantage over tech-led companies that may lack clinical-medical expertise and are positioned to excel in providing integrated healthcare solutions.

Service integration is the new innovation: Point-solution companies in areas like home care, digital therapeutics, and remote patient monitoring will grow independently for the next few years and they will increasingly collaborate with integrated players.

Value-based care shift: Shifting the focus from reactive to proactive healthcare will drive the adoption of value-based and outcome-based care models, emphasising high-quality healthcare outcomes.

Digital health firms are expected to evolve into preventive-predictive care partners by 2030: Companies will actively engage with individuals, leveraging technology and data driven insights to help prevent health issues before they occur and predict potential risks.

Investor activity: Total funding in the healthtech companies in India plunged 55 per cent from US$3.2bn in 2021 to US$1.4bn in 2022

Drop in healthtech funding was mainly due to a massive decline (75 per cent) in late-stage investments from $2.4bn in 2021 to $606mm in 2022. Investors across the globe became cautious amid funding winter, current macro conditions, and rising interest rates. While the early-stage funding saw an increase of 26 per cent YoY to $743mm in 2022, seed-stage funding for the sector fell 52 per cent YoY to $75.2mm in 2022.

For more detailed insights, access the entire report here.