Pharma Newsletter — 2nd Edition

Key Transactions in the Last Quarter

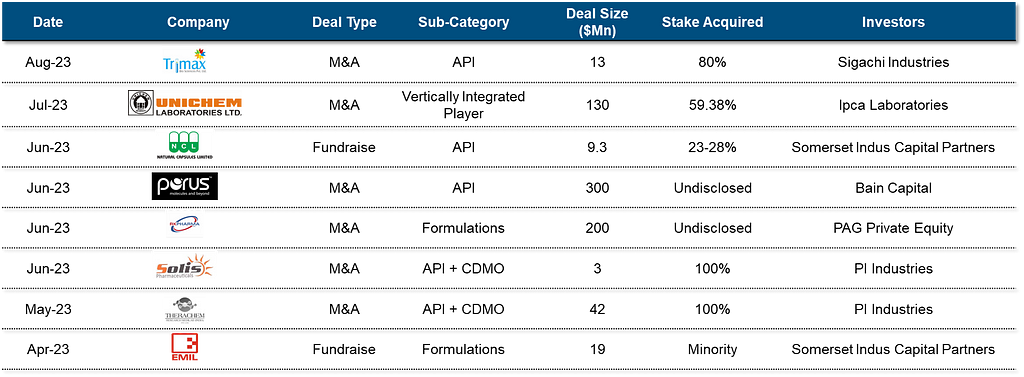

Deal value in the last quarter > $700 Mn across API and Formulations with API taking a major shareWe notice an increasing interest from PE funds in Integrated Players signaling a shift towards increasing investments in Pureplay Formulations Players & Vertically Integrated Players

Roundup of Key Deals

API as a sector continues to attract investments from Players across the Value Chain

Forward IntegrationSpecialty chemicals players have made strategic acquisitions to forward integrate into API manufacturingThe strategy is to expand their portfolio of offerings to include pharmaceutical APIs and eventually cater to regulated markets like USA and EuropeSynergies from capability acquisitions — reaction capabilities being applied to improve manufacturing processes to lower costs and thus increase competitivenessFirms are specifically looking to acquire USFDA & EUGMP approved facilities to operate in the USA, EU and other Regulated markets

2. Backward Integration

Integrated and Formulation Companies are investing in Backward Integration — there are niches within the large small molecule universe where companies are backward integrating (Ex — Steroidal APIs)

This will enable companies to

Improve cost positionDe-risk supply chains & reduce China dependenceThus increase cost competitiveness at a product level

Formulations, In-Vitro Diagnostics, and Biotech Companies will form the Next Wave of Investments in the Sector

Specialty Formulations continues to be Highly Value Accretive

There is significant opportunity in Therapy areas where treatments involve complex dosage forms (Injectable, ophthalmic, etc.) through the development and commercialization of complex productsThis space has high barriers to entry and limited competition due to the complexity of product development and commercialization

In Vitro Diagnostics (IVD) Sector

There is increasing interest in the sector due to a rapidly growing market and large potential for expansion.

The IVD market is set to grow rapidly buoyed by –

Increasing prevalence of Chronic DiseasesIncreasing use of Point-of-Care DiagnosticsRising acceptance of Personalized Medicine

Differentiated Biotechnology Companies

Companies focusing on technologies like Bio-Catalysis, Fermentation, etc. that can lower costs are can generate synergies for API & formulation players will continue to evince investor interest

PE Funds continue to stay bullish on the Pharmaceutical Sector and have started to look beyond API & CRAMS for investment opportunities

We Believe that the next 3 years will see heightened Deal Activity

New Platform Creation

With the heightened PE Interest, there is potential for the creation of 1 more API platform and at least 1 formulation platform in the next 3 years which will increase the level of consolidation in the highly fragmented market

Valuations

Valuations have seen an upward trend in the last 2 months and we expect to see a large number of deals in the next 18 months across API, CRAMS, Formulations — Domestic & Specialty

Major investments by Global PEs

Global funds like Blackstone have evinced interest in investing in a Vertically Integrated Players like Cipla and also in a CRAMS player like Sai Life SciencesThe Cipla transaction could potentially be the largest PE transaction in India across sectors and will likely set a valuation benchmark for promoters looking for an exit

Listed Company Financials — API

Listed Company Multiples — API

Insight Corner — The Case for a Platform Play in Formulations CMO

The Case for a Platform Play in Formulations CMO

Synergies & Moat

A common commercial platform can create significant value through bolt-on acquisitions of manufacturing facilities by bringing in business and driving up overall capacity utilization — these facilities will come with existing relationships that can be leveraged for value creation through cross-sellingCost synergies due to elimination of common overheadsPotential tax and debt synergiesGetting a USFDA / EUGMP approval for a manufacturing facility is an arduous task, thus acting as a barrier to entry to smaller players

USPs of the Platform

Business Development (BD) remains the biggest challenge for small — mid sized players with strong technical capabilities and regulatory track record and this can become a core differentiatorPotential to become a one-stop shop for chosen Niches (Dosage forms, therapy areas, end-markets, etc.)Better Asset Utilization due to more efficient Business Development